Here at the Trading Gurus we often get asked to write MetaTrader 4 "robots". When asked "how much" we quote a random large number. We then add the rider "If you don't mind making your robot open source and letting us publish it on our community forum we'll do the job pro bono". Nobody has ever taken us up on either of our generous offers. Until now that is!

The man who has broken the mould is called Shing Tat Chung, who is currently a student of design at the Royal College of Art in London. For his part he gave us a specification for a "superstitious robot", which we ultimately agreed should be christened "Sid". For our part we delivered an MQL4 expert advisor, which you can now download from the "Sid the Superstitious Robot" thread on the Trading Gurus community forum.

Shing has not only designed Sid's superstitious trading algorithm, but also the "Superstitious Fund" that Sid is currently managing as well. Sid even has a "Big Board" of his very own, also designed and built by Shing. As you can see, it displays in real-time the current value of the Superstitious Fund plus some additional information:

")

The Superstitious Fund's live performance board. (Image by Diego Trujillo)

If you would like to see Sid and his Big Board "in the flesh" they are being exhibited at Testbed 1 on the RCA's Battersea campus for the next few days. Sid will continue to manage the Superstitious Fund until June 1st 2013.

Any questions? Here's Sid's very own thread once again!

Last but not necessarily least, and just in case this provides a straightforward answer to your question:

Sid is sponsored by Trading-Gurus.com and supported by Microsoft Research, UK.

Filed under Trading Systems by ![]()

I've just found myself engaged in an interesting conversation over at LinkedIn concerning the oft posed question that:

There appears to be a high variance for order throughput times [when using] QuickFIX[/J]

The LMAX multilateral trading facility is written 100% in Java, and here's a presentation that I attended last year given by their then chief technology officer Martin Thompson:

Martin discusses much of the "folklore" concerning what's involved in persuading Java to trade at an ultra high frequency, and at around 16:40 he observes that:

If you try to get anywhere near 39,000 price updates a second through QuickFIX/J I'd love to see the processor you pick to do it on. It's a great FIX engine, it's reliable, it's reasonably stable, it generates a huge amount of garbage and it does horrendous things from a performance perspective. Have a look at the code for how it parses an integer.

Your application may well not be as demanding as an MTF, but what's your experience with QuickFIX/J? Are you impressed by its reliability and stability, or are you frustrated by its inconsistent latency and therefore willing to pay good money to get greater consistency?

Filed under Trading Platforms by ![]()

Fresh from prosecuting and fining a range of foreign exchange brokers the CFTC have now started to fry some bigger fish. Referring to a by now familiar misuse of supposedly segregated funds, and using a by now familiar form of words, they just announced that they have:

Filed and simultaneously settled charges against JPMorgan Chase Bank, N.A. (JPMorgan) for its unlawful handling of Lehman Brothers, Inc.’s (LBI) customer segregated funds.

Do you remember Lehman Brothers? It seems that the CFTC:

Finds that from at least November 2006 to September 2008, JPMorgan was a depository institution serving LBI, a futures commission merchant (FCM) registered with the CFTC. During this time, LBI deposited its customers’ segregated funds with JPMorgan in large amounts that varied in size, but almost always more than $250 million at any one time.

During the same time period, JPMorgan extended intra-day credit to LBI on a daily basis to facilitate LBI’s proprietary transactions, including repurchase agreements, or “repos.” JPMorgan would extend intra-day credit to LBI to the extent that LBI’s “net free equity” at JPMorgan was positive. As of November 17, 2006, JPMorgan included LBI’s customer segregated funds in its calculation of LBI’s net free equity, even though these funds belonged to LBI’s customers

This sort of behaviour is prohibited by the Commodity Exchange Act (CEA) but it happened anyway, so:

The CFTC order imposes a $20 million civil monetary penalty against JPMorgan. The order also requires JPMorgan to implement undertakings to ensure the proper handling of customer segregated funds in the future and to release customer funds upon notice and instruction from the CFTC.

In another announcement earlier this week the CFTC filed, but just for a change didn't settle, charges against:

The Royal Bank of Canada (RBC), a Canadian bank and financial services firm doing business in New York, with conducting a multi-hundred million dollar wash sale scheme in connection with exchange-traded stock futures contracts.

In this case it seems that the Royal Bank of Canada is going to contest the CFTC allegations that:

From at least June 2007 to May 2010, RBC allegedly non-competitively traded hundreds of millions of dollars’ worth of narrow based stock index futures (NBI) and single stock futures (SSF) contracts with two of its subsidiaries that RBC reported as “block” trades on OneChicago. The CFTC’s complaint alleges that RBC’s NBI and SSF trading activity, which accounted for the majority of OneChicago’s volume during the relevant period, constituted unlawful non-competitive trades, wash sales and fictitious sales.

I wonder what other tricks the CFTC might have up its sleeve, particularly with elections on the horizon in the not too distant future? They themselves put it this way:

Today’s action should make clear that the CFTC will not hesitate to bring charges against even the most sophisticated market participants who unlawfully exploit the futures markets for their own gain.

Filed under Regulation by ![]()

A mere two and half years after it was first released for public testing it is now possible to trade live on MetaTrader 5 using an FSA regulated broker. Today Alpari announced that:

Alpari (UK) launches the live MetaTrader 5 (MT5) platform with market depth and one-click trading.

To go with the new platform Alpari have also introduced a new "ECN account". According to their website opening one will allow you to:

Take full advantage of non-dealing desk execution, market depth, one-click trading, 1:500 leverage and spreads from 0 with no re-quotes.

The minimum deposit is $200, the maximum leverage is 500:1 and micro-lots are available also. Instruments are currently limited to spot FX and precious metals. Trades will be commission free until July 2nd, when prices will go up!

Alpari aren't the first UK broker to go live with MT5 however. ActivTrades did that a few weeks ago, and unlike Alpari they offer spread betting using MetaTrader 5, as well as spot forex and a range of index and commodity CFDs. We've already added ActivTrades MT5 to our long term spread betting comparison test, and we'll also be testing these new Alpari ECN accounts along with LMAX MTF accounts in similar fashion.

As a taster, here's a comparison of spreads from Alpari MT5, ActivTrades SB MT5 and LMAX MT4:

Spread comparison for Alpari ECN, ActivTrades spreadbet and LMAX MT4

Finally, for the moment at least, here's what cable's depth of market from a variety of brokers looked like earlier this evening:

Depth of market comparison for Alpari ECN, Dukascopy and LMAX

Alpari ECN on the left, Dukascopy ECN in the middle, and LMAX MTF on the right. Dukascopy's numbers are in mio, and LMAX's in their standard 10k lots. Which out of that little lot most takes your fancy at this juncture?

Filed under Brokers by ![]()

Waiting for me in my inbox this morning was an email from OANDA informing me that:

The OANDA team is pleased to announce the launch of Contract for Difference (CFD) trading on the OANDA platform.

That was sufficient to persuade me to fire up fxTrade, which duly invited me to add some new symbols to my list. Having done so, this is what my quote window now looks like:

OANDA quotes, now with added indices and commodities

Filed under Brokers by ![]()

WorldSpreads are (or perhaps I should say were?) an AIM listed spread betting broker, famous in this part of the world for offering "zero spreads" on some popular instruments as long as you sent them £5000 up front. This morning their website has taken on a whole new look. After an obviously hasty redesign over the weekend it now says:

Upon the application of the directors of WorldSpreads Limited, the High Court has today appointed Jane Moriarty and Samantha Bewick of KPMG LLP as joint special administrators of WorldSpreads Limited, under the Special Administration Regime (SAR). WorldSpreads Limited is a wholly owned subsidiary of WorldSpreads plc, a company incorporated in Dublin, Ireland.

The administration of Worldspreads Limited follows the discovery of accounting regularities which the company became aware of during the course of Friday 16 March 2012. Following this it quickly became apparent that there was a shortfall in client monies and the directors and their advisors concluded that the best course of action, in order to mitigate losses for clients, would be to place the company into special administration.

In events rather reminiscent of the MF Global fiasco, albeit on a smaller scale, it now seems as though it might take quite a while for WorldSpreads customers to be able to withdraw any money from their accounts. We will watch with interest to see whether British and Irish law is any more effective at returning supposedly "segregated" funds to their rightful owners than United States law has thus far proved to be.

I wonder how much will be left in the pot after the special administrators and other legal eagles have taken their cut, and how much the Financial Services Compensation Scheme (FSCS for short) will eventually cough up. According to The Financial Services Authority (FSA for short):

The joint special administrators will review the client cash holdings positions and will return as much cash as possible directly to each client as soon as practicable. However, clients should be aware that any shortfall in the client money accounts will impact the amount of money that can be returned.

Depending on individual circumstances customers may have access to the Financial Services Compensation Scheme (FSCS) should there be any losses. Customers should contact the special administrators to understand more about implications for them personally.

Customers of WorldSpreads should contact the joint special administrators for more information on 020 3284 8829.

Filed under Brokers by ![]()

We've previously discussed a variety of academic and political views on the costs and/or benefits of high frequency trading here on the Trading Gurus blog. If that type of thing is of interest to you as well then you might want to wander over to The Economist, where a "virtual debate" is currently taking place on the topic of "This house believes that high-frequency trading contributes to the overall quality of markets".

Proposing that motion is Jim Overdahl, currently vice-president of the Securities and Finance Practice, National Economic Research Associates, and ex SEC and CFTC. His opponent in the debate is Seth Merrin, serial entrepreneur and currently CEO of Liquidnet. As some commentators over at the Economist have pointed out, these guys might not be entirely unbiased! Despite that I'm finding the discussion very interesting, with lots of links to learned economists' findings that support both sides of the argument. There are also lots of pertinent views being expressed from practitioners on the "virtual floor". Here's a few snippets to give you a flavour. For some reason the guys at the front seem to be much more focussed on stocks rather than commodity futures, so firstly lets hear from a "hedger" in the agricultural markets, who seems to be anti HFT:

When a farmer hedges the fall soybean crop, the slippage or range of hedging prices has almost doubled to what it was five years ago. The HFT markets has scared a lot of REAL users OUT of the market place.

On the other side of the fence here's someone who sounds like he's an "investor" in stocks:

If you think about how stock trading was done 10-20 years ago by banks over the phone, and later through internet brokers and public exchanges, you'll see that a typical HFT earns much less than the fat fees banks used to charge or fees a typical internet broker charges. Today's markets are much more transparent and efficient thanks to computer automation and HFTs. I believe nobody should expect us to go back to the 'stone age' days of trading.

The Economist's debate still has a few days to run, with the closing arguments being put forward next week. Currently the voting is 42% in agreement with the motion, and 58% against. However that vote finishes up, I feel sure that this one is going to run and run. Politicians and regulators will ultimately have much more to say on the issue than even The Economist and its readers.

Filed under Regulation by ![]()

For the last month or so Ray the Random Robot™ has been involved in a friendly competition with RAI, a cousin of his conceived in the laboratory of Dr. T, who installed some artificial intelligence in the space between the ears where Ray keeps his artificial stupidity. Both "robots" were entered in the February 2012 Vantage FX/myfxbook trading contest, and myfxbook have just announced the final results on their blog. Having read that blog post, and then checked his own final standing in the competition, Ray is now suffering from a terrible pain in all the diodes down his left side and is hiding in a corner of his room. He's refusing to talk to anyone, least of all me. I'll try to explain on Ray's behalf the cause of his current psychological problems.

Only a few short days ago things looked so much brighter for him, and Ray was quietly confident of being in front of RAI by the time the final whistle blew. The competition rules stated that:

- All open positions will be automatically liquidated at the end of the contest.

- The top 3 placed participants of the contest are those with the highest percentage gain at the end of the contest period, after liquidation.

On top of that it was only on February 20th when myfxbook announced, again on their blog, that:

We’re excited to announce a very anticipated and requested change – equity based drawdown. As you might know, the drawdown calculation up until now was balance based, however that isn’t the most accurate way of measuring drawdown since equity can move drastically while the balance remains the same.

Quite so! However despite all those fine words, according to the table of results of the competition on the myfxbook site this morning Ray is in 175th position out of 2700, with a "gain" of 51.09% over the month:

Ray the Random Robot finishes the myfxbook/Vantage FX trading contest in 175th position

whereas RAI is up in 111th position with a "gain" of 81.23%:

RAI the Robot finishes the myfxbook/Vantage FX trading contest in 111th position

There was some sort of technical glitch at the start of the second week of the contest, and it now looks as though there was another one at the last moment also. None of Ray's final six trades were liquidated at the end of the contest, and it seems as though the same thing applied to all the other contestants too. If the rules had been adhered to he would actually have finished the contest with an equity gain of 35.5% following a maximum equity drawdown of 29.11%, compared to RAI's final equity loss of 20.53% following a drawdown of 77%. The winners did much better than either Ray or RAI of course. Here's how the top ten got on:

The balance curves of the top ten competitors in the myfxbook/Vantage FX trading contest

The winner achieved a monthly gain of 5254.37% following a drawdown of 79.13%. Now that I've put the record straight on his behalf I hope Ray will emerge from his self imposed isolation and start talking to RAI and I again very soon. After all, there is another myfxbook MetaTrader trading competition starting in a few days time and, as they themselves point out, there is "zero risk" and "you have nothing to lose".

Let's all hope things run a bit more smoothly next time around.

Filed under Trading Contests by ![]()

Earlier this week LMAX (who have now started to refer to themselves as LMAX Exchange instead of LMAX Trader) quietly started allowing existing customers to trade on their multilateral trading facility using MetaTrader 4, but they're not advertising that fact!

Whilst the platform is the same old MT4 that you may well be familiar with, other aspects of trading at LMAX using MetaTrader will almost certainly not be what you're used to. For example, currently LMAX do not offer demo accounts and to start live trading you firstly need to open an LMAX Classic account with a minimum of $10,000. Having done that you can then ask LMAX to transfer part of your deposit to an LMAX MT4 trading account, and start trading at a minimum size of one standard LMAX lot (10,000 units of the underlying currency, equivalent to a MetaTrader "mini-lot") with leverage of 100:1.

Unable to resist such a temptation I transferred £500 from my main LMAX account yesterday and then installed LMAX MT4 on our UK VPS. The MT4 setup program provided by LMAX proved to be unbranded, but once installed it became evident that LMAX are actually using bridge technology supplied by PrimeXM. Next I copied the latest version of Ray Robot II into the newly created experts folder, and then set him running on a daily chart of GBP/USD shortly after 11 PM last night, with exactly the same settings as he's using in our long term MT4 spread betting test. By lunchtime today this is how things looked:

LMAX MetaTrader chart for GBP/USD on March 2nd 2012

The first thing to notice is that the chart contains every daily bar of historical data that LMAX currently provide, so doing much in the way of backtesting is going to be rather tricky! Secondly, LMAX's flavour of MT4 runs on UK time rather than European time. As luck would have it "yesterday's" high and low came out roughly the same at LMAX, Alpari and GKFX, but we'll have to tinker a bit with Ray's inner workings in an endeavour to better compare like with like in the future.

When the screenshot shown above was taken Ray was already short, and a bit later in the day his 50 pip target was reached, revealing another thing not often seen in a MetaTrader 4 screenshot:

Ray pays 50 pence commission on his first live LMAX MT4 trade

As you can see, Ray had to part with 50p in commission on his first trade, but at least he had the consolation that this unusual overhead came out of the proceeds of a profitable first trade rather than his deposit. If you look very carefully you might also notice that Ray profited from sufficient positive slippage on his limit order exit to cover that commission.

Another consolation that you might expect for paying commission is lower spreads, and here's a snapshot of how LMAX's looked in the early afternoon today:

Some sample LMAX MetaTrader 4 quotes on the afternoon of March 2nd 2012

0.9 pips on cable is certainly less than Ray is used to paying on his other live test accounts. In total 30 FX pairs are available, plus gold and silver as you can see. No CFDs as yet though.

If you're a MetaTrader fan and you like what you've seen so far of LMAX's flavour of MT4, but you don't have $10,000 available to tie up while you evaluate it, there are one or two options open to you. LMAX assure me that (for the moment at least) if you're willing and able to deposit $1,000 with them they will allow you to evaluate their new platform in live trading, but they will expect you to deposit an additional $9,000 in due course if you decide trade through them long term.

Alternatively you might prefer to visit the website of Estonian broker Armada Markets, on which they say that "LMAX connectivity gives our clients exclusive access to extremely tight spreads, unmatched liquidity, speed of execution and pricing transparency", and where they offer more conventional free MetaTrader demo accounts. Armada's "primeExchange" account sounds a lot like LMAX's own MetaTrader account with added "micro-lots" and slightly lower commissions, whereas their "primeClassic" account has significantly wider spreads, but no commissions whatsoever and maximum leverage of 500:1.

Filed under Brokers by ![]()

Ray Robot II™ has now been running his live spread betting test comparing Alpari UK with GKFX for over a month. We're rather obsessive here at the Trading Gurus, and we've noticed a variety of interesting differences between Ray's four experimental accounts during that time. Some observers have however suggested to us that all that matters in a trading account is "the bottom line". Whilst we humbly disagree with that assertion, Ray is nonetheless now proud to announce that there is at last a difference between the bottom line of his Alpari accounts (currently standing at £255.00) and his GKFX accounts (currently standing at £261.00). There are any number of other (less significant?) differences also.

Let's first of all compare equity curves for Ray's live accounts. Here's how his Alpari UK spread betting account looks this morning:

Ray Robot's live equity curve on December 21st 2011 at Alpari UK

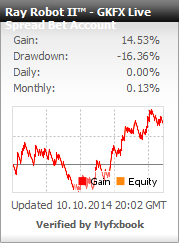

According to myfxbook the bottom line of £255 can be characterised by a "Profit Factor" of 1.25 following a "Drawdown" of 3.85%. Now here's Ray's GKFX equity curve:

Ray Robot's live equity curve on December 21st 2011 at GKFX

According to myfxbook once more this time around Ray's profit factor is 1.58 after a drawdown of 3.46%. Here's a funny thing though. If you look at Ray's trading accounts at Forex Factory instead of at myfxbook the drawdown numbers are slightly different. Here's another funny thing too. This morning I ran some backtests on the same two accounts, on the same VPS, over the same period of time. Here's what the MetaTrader 4 strategy tester showed me, first for Alpari:

Ray Robot's backtest results on December 21st 2011 at Alpari UK

As you can see, in backtests Alpari's version of MetaTrader reports a profit factor of 2.81 following a drawdown of 2.92%. Taking a look at GKFX instead:

Ray Robot's backtest results on December 21st 2011 at GKFX

As you can see, we have yet another different equity curve, and another set of numbers. This time we're told the profit factor is 2.50 and the drawdown is 4.08%.

Here's an entertaining game for any interested readers to play over the Christmas holiday season. Which of all those different sets of results do you think best represents Ray's future performance trading cable in the New Year? Finally, if you should happen to have some spare cash left over after doing all your Xmas shopping, on the evidence Ray has accumulated so far in his testing would you prefer to open a spread betting account with Alpari UK or GKFX?

Filed under Brokers by ![]()