Regular readers will recall that we reported back in 2011 that IBFX had been acquired by TradeStation, itself part of the Japanese Monex Group. Now it looks as though Monex has finished its brief excursion into MetaTrader land. I've received several emails announcing the news summarised in today's headline. According to FXCM's news release:

FXCM Holdings LLC, has signed a definitive agreement with IBFX, Inc. and IBFX Australia Pty Ltd to acquire their U.S. and Australian MetaTrader 4 retail forex accounts.

FXCM will be acquiring approximately $63 million in client equity and 13,000 accounts.

Financial terms of the transaction were not disclosed at this time.

Meanwhile I also received an email from IBFX advising me that:

IBFX Australia Pty Ltd. recently agreed to transfer your current IBFX “MT4” account to FXCM Australia Ltd. The transfer is scheduled to take place beginning the weekend of September 19, 2014. FXCM holds an Australian Financial Service (“AFS”) license issued by the Australian Securities and Investments Commission (ASFL No. 309763).

If you have no objection to the transfer of your account to FXCM, then no action is required. You have the right to opt out of the transfer, but because IBFX has made a business decision no longer to service individual MT4 online platform accounts, if you do opt out, then on September 19, 2014 all open positions in your account will be liquidated via market orders and, once that has been completed, appropriate steps will be taken to close your account.

Meanwhile FXCM Australia Limited sent me an email referring me to their "IBFX Transfer Center", which tells me that:

FXCM is transferring clients to No Dealing Desk with lower spreads plus a commission.

Nano Lots on open positions will be closed at market price. Please manage nano lots accordingly. The smallest lot offered by FXCM will be Micro (1k) lots through our No-Dealing Desk Execution.

Since the existence of nano lots was the sole reason that I originally opened an IBFX account it sounds as though my best option will be to object to FXCM's generous offer!

Filed under Blog by ![]()

I don't know about you, but here at the Trading Gurus HQ (TGHQ for short) we've been receiving a veritable blizzard of emails recently saying things like:

Dear Trader,

Please be aware that we have been informed by Meta Quotes that as from Friday 1st August 2014 all clients using a version of MT4 older than Build 600 will not be able to use it, as it will be disabled.

Please ensure you are using a current version.

MetaTrader 4 build 600 was released back in February, and according to MetaQuotes' slightly stilted English in their news release:

MQL4 language for programming trading strategies has been substantially revised and its functionality has been brought closer to that of MQL5. Classes and structures have been added and the language syntax has been extended up to С++ level allowing developers to implement all the advantages of object-oriented programming.

It means that trading robots and technical indicators can be created much easier and faster now, while Expert Advisor developers have gained new opportunities in a single MetaEditor development environment – debugging, profiling, code completion, etc.

That means that any active MT4 user out there should be using an OOP capable version by now. Here at the Trading Gurus that has got us all very excited, because it means that we can now say things like this:

If you have an unusual requirement such as getting FIX 4.2 talking to MT4 over a wide area network using JSON over Google protocol buffers and/or 0MQ then please do not hesitate to get in touch.

To get an idea of just how many people currently need to take heed of all those emails on Friday afternoon I called Paul Hare, Director of Trading at UK broker GKFX. He told me that:

Out of a total of over 30,000 clients only around 250 are still not on build 600 or above.

If you haven't upgraded yet please do so now. You know it makes sense!

Filed under Trading Platforms by ![]()

Regular readers of the Trading Gurus blog will be aware that we have been pondering the possible effects of additional regulation on markets on both sides of the Atlantic for some considerable time now. In this guest post Alex Krishtop of Edgesense Solutions speculates about what the future holds for the world's financial markets. In our view Alex's crystal ball is much clearer than those of the vast majority of market commentators.

For more than a year regulators on the both sides of Atlantic have been working hard applying new restrictions to many different markets. The swaps market was possibly the first to undergo major changes. Then followed other derivatives and most OTC markets in general. Attacks on HFT are another substantial segment of modern regulatory activity. The spot FX market was also not left untouched: severe restrictions on banks’ prop activity have already caused a serious restructuring of the whole business and generated a great number of job seekers, but with the most recent proposals by the Financial Stability Board it’s now not unlikely that a centralized clearing facility will be established for this largest OTC market (so far).

What are the consequences of all this unprecedented activity and who are its real beneficiaries?

The average Joe might think that all these measures are indeed intended to reduce “market manipulation” and therefore to “protect” something, his pension savings for example. Probably this is the official decoration for all these processes. We should note here that the chances are, though, that the average Joe won’t ever understand what this campaign is all about. However he doesn’t need to.

Looking at these processes more critically one could easily note that all of them imply greater centralization of all markets and an increasing role for the exchanges and central clearing houses (and similar centralised structures). Therefore the regulatory process probably serves the interests of the exchanges and large brokers. As an immediate effect it causes increased expenses (considering just the new reporting requirements — not every institution would be able to afford it!), and as a consequence — increased transactional costs, at least for most trading venues. As the result, only the really big players in this market will be able to afford to conform to the new rules of the game. Therefore their importance will increase further while minor market participants are likely to further lose their share.

Now what is there in this analysis that could be useful for market speculators? Presently the market is right in the middle of the process of restructuring, and when this process is over we will see a completely new world. The fact that the market is currently in transition is most likely the very reason for the unprecedentedly low volatility, and understanding this reason helps one to estimate how long it might last. With the increased transactional costs we can expect the “come-back” of trading in underlying instruments instead of derivatives, with possible a greater focus on commodities. Besides that the new environment may significantly diminish the reward/risk ratio for many (if not most) short-term and ultra-short-term strategies, along with “market neutral” strategies. In other words, everything that used to generate 20% annual profits with virtually zero risk (“a new standard”, as one of my friends said) might well be rendered useless.

However the most likely and most influential outcome of the whole process will be dramatic reduction of liquidity in all markets, but especially in FX, that will lead to increased volatility and in general a result that is diametrically opposed to that declared by the regulators. Then we might expect the volatility-based alpha-generating strategies to celebrate the “great come-back”.

It’s especially interesting that the end of restructuring of markets will most likely coincide with the end of tapering, QE and ZIRP. This may lead to even more interesting market phenomena.

In conclusion, please don’t throw away your old breakout strategies just yet!

Filed under Guest Posts by ![]()

Ray Robot II and I have just been called a variety of names over on a LinkedIn thread started by Marcos López de Prado and entitled "Pseudo-Mathematics and Financial Charlatanism". As best as I can work out Guy Fleury has suffered a total sense of humour failure, and his view can be summarised as:

I remember having to wait about nine months for Ray's inevitable demise while you were praising day in and day out the prowess exhibited by your KISS randomly trading robot. When Ray blew up, which is equivalent of having lost all the money in the trading account, you gave it an educational spin. Sure… And here you are at it again.

and

You've promoted the KISS principle for some time, maybe it's time you start looking at more complicated trading structures.

For the uninitiated KISS stands for "Keep It Simple Stupid". I will happily admit that Ray Robot Jr. is simple, and his late lamented father, Ray the Random Robot, was "stupid" by design. The Son of Ray and I cannot possibly allow this wholly unwarranted slur on Ray Senior's good name to pass unchallenged. Earlier this morning I logged in to our "City of London" VPS and ran a backtest of RR2 over the same period of time that he has been live trading a spreadbet account at GKFX Spread Trading. Here is a screenshot of what was revealed to me by MetaTrader 4 version 4.00 build 625:

Screenshot revealing Ray Robot II's simulated equity curve from November 13th 2011 until April 19th 2014

Here is another graph also produced by MetaTrader 4 earlier this morning, revealing Ray's actual live trading equity curve:

Screenshot revealing Ray Robot II's live trading equity curve from November 13th 2011 until April 19th 2014

Would anyone care to play "spot the difference" with Ray Junior and I? If, unlike Guy, you would care to experiment with Ray for yourself, here is a little package we put together many moons ago that contains Ray's MQL4 source code amongst other things.

Filed under Trading Systems by ![]()

Interactive Brokers have recently released build 944 of their venerable Trader Workstation platform (or TWS for short). They have also made the interesting announcement that:

MultiCharts advanced charting is now accessible from within TWS as a complement/upgrade to our existing interactive charts.

Multicharts.net

The MultiCharts.net tool is available free of charge to IB customers (does not include the ability to trade) and includes:

- Advanced charting

- Drawing tools and a large library of more than 300 indicators

- User-programmable technical indicators

- Strategy backtesting

- User-programmable trading strategy signals

User-programmable features can be programmed using C# or Visual Basic. To trade from within MultiCharts.net, upgrade for $39.00 per month (following a one-month free trial).

MultiCharts PowerLanguage

Customers who want to trade from within MultiCharts AND who need to program complex custom technical indicators but are not programmers can subscribe to MultiCharts PowerLanguage. This version offers all of the charting features of MultiCharts.net plus the ability to trade, and the addition of PowerLanguage, a more user-friendly computer programming language with a small learning curve that was designed to be used by non-programmers. The PowerLanguage version is available for $39.00 per month (following a one-month free trial).

To summarise, as long as you have an account with Interactive Brokers and you don't object to running Trader Workstation on Windows instead of Linux you can now perform backtesting using the .NET version of MultiCharts at no extra charge. If you want to auto-trade with IB using either the .NET or Power Language flavours of MultiCharts you can do so for an additional $39 per month. Unable to resist the temptation I found the new "MultiCharts" option in the TWS "Analytical Tools" menu:

When I clicked it I was offered a choice of which flavour of MultiCharts to download:

Being a cheapskate I went for the TWS special edition of MC.NET and once everything was installed I tried backtesting Ray the Random Robot, only to be greeted with a very familiar sight:

Unfortunately even if MultiCharts is now more tightly integrated with Trader Workstation it's still a long job trying to download enough historical data to perform a backtest that uses more than a few days worth of one minute bars. Even if that sadly all too familiar message is still there, many other things are not. With the free of charge version of TWS MultiCharts there is no separate Quote Manager, there is no Portfolio Backtester and there are no 3D Optimization Charts. However there is at least a backtester now available bundled with TWS.

As a consequence another thing has just been added to our to do list. We'll now have to try out Ray Robot Junior with the MultiCharts.NET backtester to see if it is up to the job of producing some results that even vaguely resemble what Ray has managed to achieve in live trading!

Filed under Trading Platforms by ![]()

In a press release today FXCM have announced that:

Its U.K. subsidiaries, Forex Capital Markets Limited and FXCM Securities Limited, [have] entered into a settlement with the Financial Conduct Authority (“FCA”). The settlement addresses trade execution practices concerning the handling of price improvements on FXCM UK’s offsetting orders from August 2006 – December 2010.

Under the terms of the settlement, FXCM UK has agreed to pay fines totaling £4 million to the FCA and to provide approximately $10 million in restitution to the affected clients. FXCM recorded a reserve $15 million in the third quarter of 2013 for this matter and will record an additional $1.9 in the fourth quarter to reflect the terms of the settlement and related expenses. All clients receiving restitution will be notified within 60 days. Of the approximately $10 million being credited under this settlement, the impact on individual traders was typically very limited and averaged $3.70.

Unfortunately it doesn't sound like I'll be receiving a massive windfall any day soon! The FCA themselves have also issued a press release about the matter today, with a somewhat different emphasis to FXCM's. The FCA says that:

The Financial Conduct Authority (FCA) has fined Forex Capital Markets Ltd and FXCM Securities Ltd £4,000,000 for allowing the US based FXCM Group to withhold profits worth approximately £6 million ($9,941,970) that should have been passed on to FXCM UK’s clients.

FXCM UK also failed to tell the FCA that the US authorities were investigating another part of the FXCM Group for the same misconduct. The FCA has ensured that FXCM UK’s clients will be fully compensated, with credit automatically paid to their accounts.

According to Tracey McDermott, the FCA’s director of enforcement and financial crime:

Not only did FXCM UK fail to treat its customers fairly or correctly apply our rules, I am particularly disappointed that it was not transparent in its dealings with the FCA. We expect all firms to put customers at the heart of their business, and we have taken action to ensure clients of FXCM UK will get redress.

The FCA press release goes on to provide more details about FXCM UK's failure to treat its customers fairly, explaining that:

Between August 2006 and December 2010, the FXCM Group kept profits from favourable market movements between the time the orders were placed by FXCM UK and executed by the FXCM Group, while any losses were passed on to clients in full – a practice known as asymmetric price slippage.

As both FXCM and the FCA are at pains to point out, here in the UK at least there are rules about "best execution" that brokers are supposed to adhere to:

Brokers in certain markets, including regulated CFD and spread-bet firms and those offering Rolling Spot Forex contracts for difference, may be failing to recognise that their activities fall within the scope of the best execution rules.

Do you suppose that all those UK regulated CFD, spread-bet and FX brokers will now hastily correct any such failures?

Filed under Regulation by ![]()

As we reported way back in August, MetaQuotes have been working on adding objected oriented programming to MetaTrader 4. They originally suggested that a version of the MetaTrader 4 terminal supporting OOP EAs would become available in September, but that's not how things have worked out in practice!

After a long and frustrating wait, it has come to our attention that it is now possible to beta test object oriented MQL4 expert advisors on a MetaQuotes demo account. Here's the instructions on how to do so, translated from the original Russian by Ovo on the MQL4 forum:

- Create a new and clean MT4 installation in a new folder. You may need to Download MetaTrader 4 Terminal Installer (455 Kb)

- Try to login, with the server field set to demo.metaquotes.net:444 (which will not succeed)

- Apply for a new demo account, with the demo.metaquotes.net:444 server selected.

- Shut down the terminal. Reopen this installation of the MT4 terminal. Update of beta commences and you'll get the new beta installed.

I tried that, which worked as predicted, and I now find myself looking at MetaTrader 4 build 551 dated 29th November 2013! Having finally managed to properly test our first draft of an MQL4 object oriented expert advisor we discovered a couple of little bugs, so I've now posted a modified MQL4 version of object oriented Ray the Random Robot over on the Trading Gurus Community Forum.

Filed under Trading Platforms by ![]()

Although the Current Employment Statistics section of the United States Bureau of Labor Statistics still says:

The Employment Situation for September 2013 is scheduled to be released on October 4, 2013, at 8:30 A.M. Eastern Time.

the BLS home page currently displays this notice:

This website is currently not being updated due to the suspension of Federal government services. The last update to the site was Monday, September 30. During the shutdown period BLS will not collect data, issue reports, or respond to public inquiries. Updates to the site will start again when the Federal government resumes operations. Revised schedules will be issued as they become available.

Please visit www.opm.gov for the most recent information on Federal government suspensions, shutdowns, and closings.

It looks like tomorrow's anticipated release of the September NFP numbers will not now take place. It also looks like even Barack Obama doesn't know when everyone will be back at their desks at the BLS, and hence when their "revised schedules" might be made available. The Office of Personnel Management web site is currently showing a message from the President "to the dedicated and hard-working employees of the United States Government" dated October 1st 2013, in which he says:

The Federal Government is America's largest employer, with more than 2 million civilian workers and 1.4 million active duty military who serve in all 50 States and around the world. But Congress has failed to meet its responsibility to pass a budget before the fiscal year that begins today. And that means much of our Government must shut down effective today.

This shutdown was completely preventable. It should not have happened. And the House of Representatives can end it as soon as it follows the Senate's lead, and funds your work in the United States Government without trying to attach highly controversial and partisan measures in

the process.Hopefully, we will resolve this quickly. In the meantime, I want you to know-whether you are a young person who just joined public service because you want to make a difference, or a career employee who has dedicated your life to that pursuit-you and your families remain at the front of my mind.

Hope springs eternal, but it doesn't actually pay anybody's bills. According to the August statistics available for download from the US Treasury Direct web site, the United States total public debt outstanding on August 31st was 16,738,650 million dollars.

Filed under Economics by ![]()

In the United States the Democrat and Republican parties are still at loggerheads in Congress over "Obamacare", and as a result many "non-essential" services have been shut down, and getting on for a million US government workers have been told to stay at home. Here's a video report from Al Jazeera on the current state of the nation in the land of the free:

Note that President Obama said that:

Congress generally has to stop governing by crisis. They have to break this habit. It is a drag on the economy.

The back and forth offered no sign that President Barack Obama and Republicans can soon end a standoff over health care that has sidelined everything from trade negotiations to medical research and raised new concerns about Congress's ability to perform its most basic duties.

An even bigger battle looms in coming weeks, when Congress must raise the debt limit or risk a U.S. default that could roil global markets.

Stock investors appeared to be taking the news in their stride with investors confident a deal could be reached quickly. The S&P 500 closed up 0.8 percent and the Nasdaq Composite gained 1.2 percent. But the U.S. Treasury was forced to pay the highest interest rate in about 10 months on its short-term debt as many investors avoided bonds that would be due later this month, when the government is due to exhaust its borrowing capacity.

If Congress can agree to a new funding bill soon, the shutdown would have little impact on the world's largest economy. A week-long shutdown would slow U.S. economic growth by about 0.3 percentage points, according to Goldman Sachs, but a longer disruption could weigh on the economy more heavily as furloughed workers scale back personal spending. The last shutdown in 1995 and 1996 cost taxpayers $1.4 billion, according to congressional researchers.

I wonder what China thinks about the prospect of "a U.S. default"? Watch this space for more news, but don't hold your breath waiting for the warring parties to come to an amicable solution any time soon.

Filed under Economics by ![]()

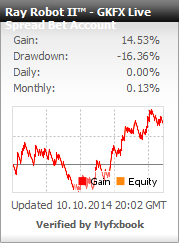

Regular readers of the Trading Gurus blog will know that the Son of Ray the Random Robot™ has been simultaneously spreadbetting a variety of live MetaTrader accounts for nearly two years now. The equity curve for his live GKFX MetaTrader 4 account can be seen to the left of this article.

Regular readers will also be aware that we've had a few problems getting MetaTrader 4 backtest results to look much like Ray Jr.'s live trading results, so in order to attempt to reduce the discrepancy we've gone back into the laboratory here at Trading Towers and created a Java clone of Ray Robot II™! This shiny new incarnation is for Dukascopy's JForex platform, and will allow us to do some backtesting using Dukascopy's tick data. Hopefully the results of those tests will look a bit more like real life than MT4's own over optimistic one minute bars! As always, the source code for the Son of Ray's latest brain transplant is available for download from the Trading Gurus Community Forum, once you've negotiated our somewhat cumbersome anti spambot procedures.

Here's a quick preview of what Ray's backtest results look like on the JForex platform:

Ray Robot II shorts cable on August 30th 2013, and makes a minor loss

As you can see, that particular trade didn't work out terribly well, but as you can also see from his equity curve Ray has somehow managed to keep his head above the turbulent trading waters for nearly two years now, and is actually on something of a winning streak just at the moment! This is how he's doing at this precise moment in time:

Ray Robot II's live GKFX equity curve on September 27th 2013

Filed under Trading Systems by ![]()